The Siren Song of the Tangible

It is a funny thing about the digital age: we spend all our time trying to invent "new" money, only to realize that the most valuable things are still the old ones like land, debt, and the steady hum of a business that actually makes something. I have spent the better part of a decade watching folks try to turn digital cats into gold mines, so when I hear the phrase "Real-World Assets" (RWA), my hand instinctively moves to cover my wallet.

But there is a flicker of sense in the RWA noise that isn't there in the latest meme-coin frenzy. If (and it is a big "if") the industry can stop trying to turn every boring treasury bond into a high-stakes gambling chip, we might actually be looking at the first piece of digital plumbing worth the price of the pipes. The goal should not be to reinvent the wheel, but to make the axle grease a little more efficient.

The High-Priced Wrapper Problem

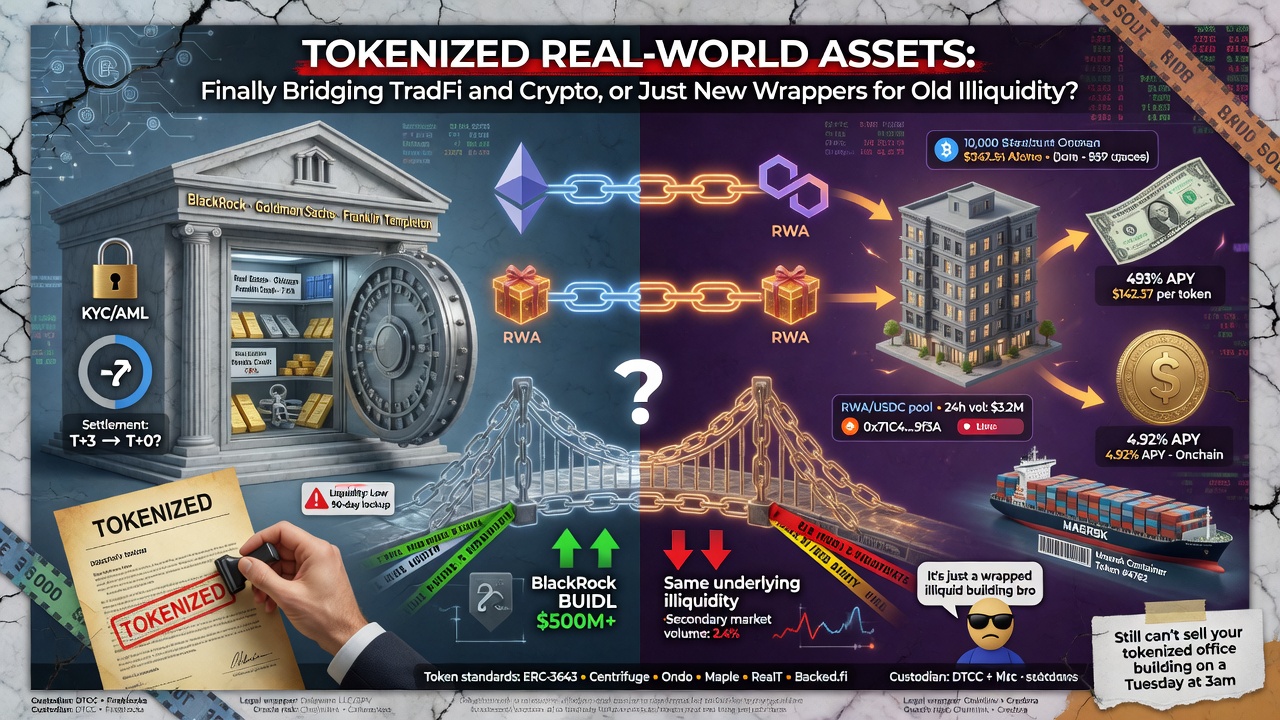

Right now, a lot of what passes for "innovation" in tokenized treasuries or real estate is really just a fancy, high-fee wrapper around a plain old ETF. If I can buy a Treasury bill for a few basis points at any reputable brokerage, why in the world would I pay a "protocol fee," a "gas fee," and a "management fee" to hold a digital mirror of that same bond? Efficiency is the only justification for technology in finance; if the new way is more expensive than the old way, it isn't progress but a grift with better marketing.

Many of these projects are over-engineered solutions to a problem that does not exist for the average investor. They promise "fractional ownership," as if buying ten dollars worth of a stock index wasn't already a solved problem in the 1990s. Unless the tokenization actually lowers the cost of the underlying asset or opens a door that was previously bolted shut, it is just a more expensive way to own the same old thing. We don't need a blockchain to tell us that a five percent yield is five percent, especially when the fees eat two percent of it on the way in.

The Mirage of Instant Liquidity

Then there is the "liquidity" tall tale. The pitch is always the same: "Trade your real estate tokens twenty-four-seven on a global market!" It sounds marvelous until you realize that a market is only liquid if there are people standing on both sides of the counter. Currently, on-chain trading volumes for these assets are about as deep as a rain puddle in July. You can put your tokenized apartment building on a blockchain, but if the only other person interested is a guy in a Discord channel with a cartoon avatar, you haven't found liquidity, but you've just found a new way to be stuck.

"A market is only liquid if there are people standing on both sides of the counter; otherwise, you're just shouting into a very expensive digital void."

True institutional adoption does not happen because you have a fast ledger; it happens when the big players trust the rules of the game. The "liquidity illusion" is a dangerous one for the retail investor. They are told they can exit at any time, but when the time comes to sell, they find that the digital secondary market has the depth of a saucer. Until the institutions bring their trillions to the chain, these tokens remain less liquid than the physical deeds they represent.

The Regulatory Tightrope and the Buffett Test

The "regulatory moat" is the only thing keeping these projects from becoming a total free-for-all, but it is also a landmine. A project that ignores the law is just a rug-pull with better vocabulary. The ones that survive will be the ones that embrace the "boring" parts of finance: KYC (Know Your Customer), AML (Anti-Money Laundering), and tax compliance. It turns out that when you are dealing with real-world assets, you have to deal with the real-world sheriff.

I always go back to what I call the Buffett Test: Would a sensible man buy this asset if the "token" part did not exist? If the answer is no and the only reason to own it is the hope that the token price will "moon", then you are not investing; you are just buying a ticket to a digital carnival. We must look for the projects quietly moving boring, cash-flowing securities, like private credit or real estate with actual, rent-paying tenants, onto more efficient rails. If it doesn't make sense in a ledger book, it won't make sense on a blockchain.

Building Railroads, Not Whistles

The real winners in this space won't be the ones promising twenty percent APY through "yield farming" alchemy. That is just shifting money from one pocket to another until the coat disappears. The real winners will be those who use this technology to strip away the middleman's bloat from a six percent mortgage or a municipal bond. We need to stop looking for the next "disruption" and start looking for the next optimization.

In the end, if the technology actually makes a boring, cash-yielding asset easier to settle and move, then you have finally stopped selling whistles and started building a railroad. The blockchain should be the invisible track, not the circus tent. Until we reach that point of maturity, I'll keep my feet on the ground and my money in things I can touch for things that have a dividend check I can understand.