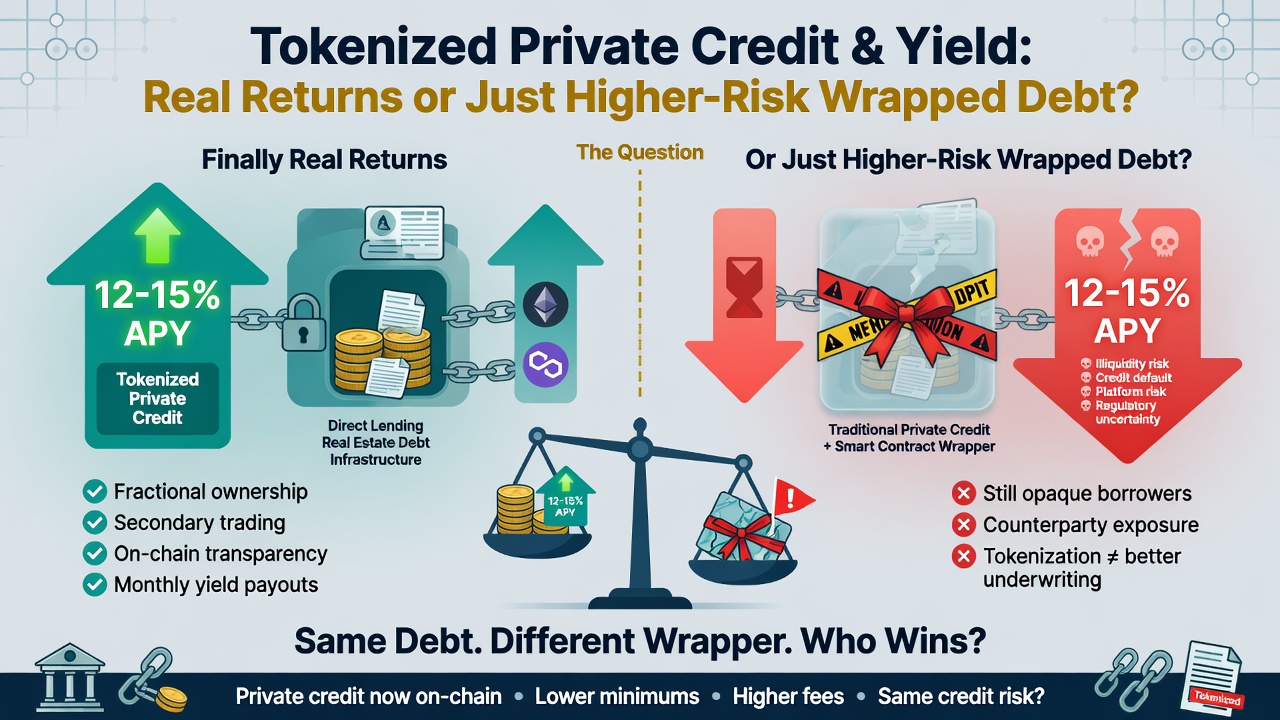

The Siren Song of Real Yield

They tell me we’ve finally found the Holy Grail of the digital age: Real Yield. The story goes that we’ve moved past the era of printing "magic beans" to reward liquidity providers and have instead plugged the blockchain directly into the pumping heart of the global economy. They call it Tokenized Private Credit. It sounds sophisticated, like something a man in a pinstriped suit would sell you over a very expensive steak. But to my eye, it looks like we’re just wrapping old, risky debt in shiny new foil and acting surprised when it still smells like a loan that might not get paid back.

The fundamental delusion here is believing that a smart contract has any jurisdiction over a man who decides he’s done paying his bills. You can tokenize a loan for a warehouse in Kansas all you like, but when the borrower stops sending checks, that smart contract doesn't have a pair of boots to kick down the door or a sheriff’s badge to seize the inventory. In my years watching the markets, I’ve learned that credit is only as good as the recovery process. In the traditional world, we have centuries of case law and physical bailiffs. In the web3 world, we have a "delegate" who promised he did the underwriting and a "pool manager" who’s likely more interested in his management fee than in chasing a defaulter through a bankruptcy court.

The Rot Beneath the Wrapper

The Federal Reserve's own records show that private credit is a murky pond even in the best of times. When "dry powder" builds up in the hands of fund managers, underwriting standards start to rot. We are currently witnessing the rise of "covenant-lite" structures where the lender has almost no right to complain until the money is already gone. Tokenizing these loans doesn’t fix the underwriting; it just democratizes the losses. It allows the sophisticated originators to offload their risk onto a retail crowd that thinks a dashboard with a 12% yield ticker is the same thing as a safe investment.

Furthermore, don't get me started on the myth of liquidity. Putting an illiquid, three-year private loan on a blockchain doesn't magically make it liquid. It just means you can see the price of your mistake update in real-time on a secondary market while you wait for a buyer who isn't coming. In a true stress event, you'll find that on-chain liquidity is about as useful as a paper umbrella in a hurricane; when everyone runs for the exit at once, the door has a nasty habit of shrinking.

The Thornewood Margin-of-Safety Framework

If you’re determined to chase this yield, you’d better bring a heavy set of scales and a very cold heart. I do not look at a credit protocol unless it passes through a quantitative meat-grinder designed to account for the inherent messiness of human failure. Here is the framework I use to evaluate any on-chain debt offering:

- The Sheriff’s Haircut (Recovery Rate): I assume a structural 50% discount on all stated collateral values. If a protocol claims a loan is backed 1:1 by real-world assets, I treat it as 0.5:1. You must account for the legal friction, court costs, and jurisdictional headaches of moving from a digital token to a physical asset.

- The Technical Premium (Yield Floor): To even merit a second glance, the yield must be at least 500 basis points (5%) above the 10-year Treasury rate. If Uncle Sam is paying 4.5% for risk-free debt, and a protocol offers you 8% for tokenized junk, you’re being paid a measly 3.5% to take on smart contract risk, platform risk, and borrower default. That’s a fool’s bargain.

- The LTV Ceiling: I won’t touch any credit pool where the Loan-to-Value (LTV) exceeds 60%. In the digital realm, where transparency is often just a smokescreen for complexity, you need that 40% cushion to survive the first sign of a market chill or a property devaluation.

The Coming Regulatory Reckoning

We must also consider the men in Washington. The regulators haven't even finished their first cup of coffee on this particular niche of the market. When the SEC eventually decides your "wrapped debt" is just an unregistered security in a cheap polyester suit, those yields will vanish under a mountain of legal fees and cease-and-desist orders. True value isn't found in the wrapper; it’s found in the cash flow and the legal right to seize the underlying asset when that flow stops.

Until these protocols can show me a digital sheriff who can actually seize a tractor in a muddy field in Nebraska, I’ll stick to the boring stuff that has a century of law behind it. The blockchain is a ledger, not a magic wand. It can record a debt, but it cannot compel a deadbeat to pay. In the end, tokenized private credit is just another way for the desperate to find yield and the cynical to find liquidity at the expense of the naive.

"Debt is a patient creditor; it doesn't care about your innovative tech. It only cares about being repaid."