I’ve spent my life looking at dirt, but Rhenium (chemical symbol Re) is something else entirely. It is the wallflower of the periodic table: it's quiet, incredibly rare, and the last stable element we actually managed to find. It wasn’t until 1925 that Walter Noddack and his team in Germany finally pinned it down. It is a refractory metal, which is a fancy way of saying it has a melting point that would make a blowtorch weep, sitting at over 5,700 degrees Fahrenheit. Only tungsten and carbon can take more heat without turning into a puddle.

The Ultimate Hitchhiker

You don’t just go out and find a "Rhenium mine." In all my years of prospecting, I’ve never seen a vein of the stuff. It is a hitchhiker. We get it almost exclusively as a by-product from roasting molybdenum concentrates, which themselves usually come from big copper pits. If you aren’t digging for copper, you aren’t finding Rhenium.

Chile is the undisputed king here, sitting on about 52% of the global supply. The U.S., Poland, and Kazakhstan pick up the rest of the slack. When it comes to refining, Chile’s Molymet and Poland’s KGHM do the heavy lifting. They turn that industrial dust into the high-purity pellets and powder the world craves. Without those specific processing plants, the raw ore is just expensive gravel.

Holding the Line at 30,000 Feet

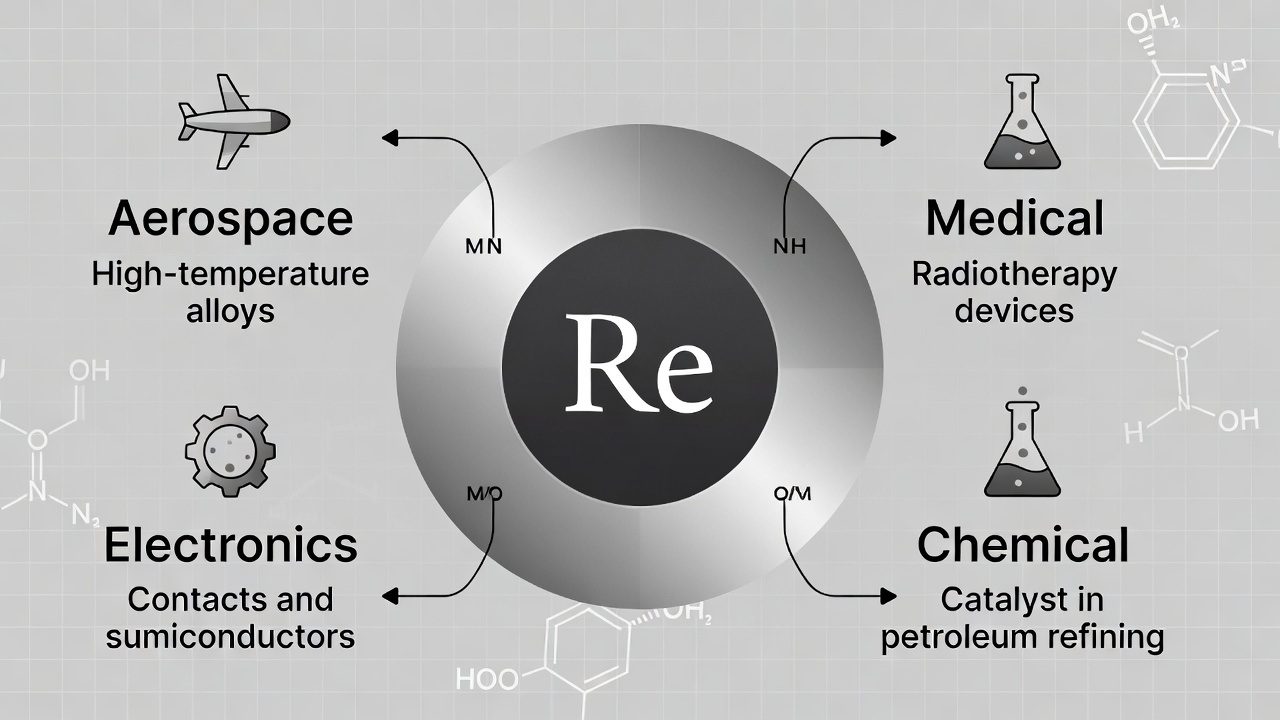

Right now in 2026, the supply-demand balance is tighter than a new pair of boots. About 58% of all Rhenium goes straight into the belly of the beast: aerospace. It is the secret sauce in nickel-based superalloys. Without it, those single-crystal turbine blades in jet engines would soften and fail under the extreme heat required for modern efficiency. If you want to fly across the ocean without the engine melting off the wing, you need Rhenium.

The rest of the market is mostly about catalysts. About 27% of the supply goes into making high-octane, lead-free gasoline. It’s also starting to show up in the hydrogen economy, where researchers are looking at it for specialty catalysts that can handle the stress of new energy production. It’s a small market, but it’s a vital one.

"Since we can’t just mine more Rhenium without mining more Copper or Moly, our supply is at the mercy of global commodity prices that have nothing to do with jet engines."

The Ten-Year Squeeze

Looking out over the next decade, demand is only going one way. Between the boom in commercial flight and the military’s constant need for higher performance, we’re looking at a serious supply crunch by the early 2030s. We are currently using almost everything we dig up, and the secondary market of recycling old engine parts is the only thing keeping the lights on.

The U.S. treats Rhenium as a strategic heavy-hitter because, without it, our Air Force stays on the tarmac. Our long-term strategy involves the Strategic National Stockpile and a frantic push for better recycling techniques. We have to learn how to pull every milligram out of spent engine blades because we can't just flip a switch and produce more.

The By-Product Trap

The most critical issue we face isn't just the scarcity; it’s what I call the "by-product trap." Because Rhenium is a secondary find, its availability depends entirely on the health of the copper and molybdenum markets. If copper prices tank and the big pits slow down production, our Rhenium supply vanishes regardless of how much the aerospace industry is willing to pay.

It’s a precarious way to run a superpower, depending on the price of copper pipe to ensure we can build jet fighters. We’re working on ways to extract it more efficiently from lower-grade ores, but that’s a long road. For now, we're stuck playing a high-stakes game of keep-away with a metal that most people have never even heard of. It’s a tough way to make a living, but as I always say, the best treasures are usually the hardest to keep.